How to Use the 50/30/20 Budget Practically in Daily Life

The Power of the 50/30/20 Budgeting Method

Many individuals struggle with managing their finances, often feeling bogged down by complexities that could easily be simplified. The 50/30/20 budget offers a practical solution, breaking down your income into manageable portions that promote clarity and control over spending habits while fostering long-term financial health.

This budgeting method categorizes your after-tax income into three key areas, allowing you to prioritize your financial commitments efficiently:

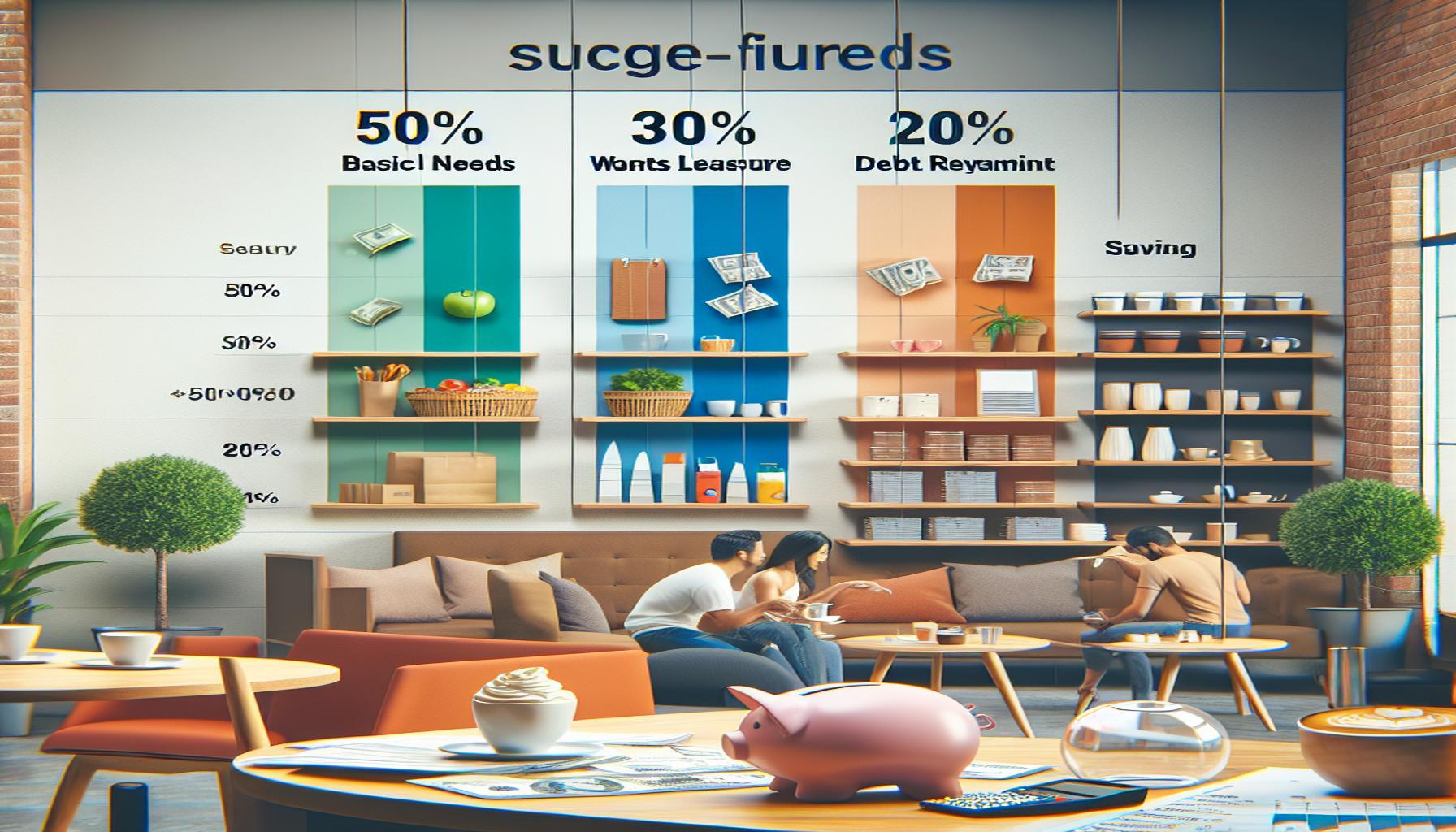

- 50% for needs: This portion covers essential expenses that are unavoidable for daily living. These include housing costs such as rent or mortgage payments, utilities like electricity and water, grocery bills for nourishment, a reliable transportation system, and healthcare expenditures. For instance, if your monthly income amounts to $4,000 after taxes, then allocating $2,000 to these essential needs ensures that you can cover life’s fundamental requirements.

- 30% for wants: This segment is focused on discretionary spending that enhances your quality of life but isn’t essential for survival. Items in this category might include going out for dinner, attending concerts, subscriptions to streaming services, or taking vacation trips. For example, setting aside $1,200 for such pleasures allows for a balanced lifestyle that doesn’t feel overly restrictive while still keeping overall spending in check.

- 20% for savings and debt repayment: The final portion emphasizes the importance of planning for your future and managing existing debts. This means contributing to retirement accounts like 401(k)s or IRAs, building an emergency fund to handle unexpected financial emergencies, and actively working on paying off debts such as student loans or credit cards. In our previous example, this leaves you with $800 to secure your financial goal.

Incorporating the 50/30/20 framework into your life can feel liberating, especially as it fosters a disciplined financial mindset while reducing anxiety surrounding money matters. Not only does it allow you to keep tabs on your spending, but it also energizes your saving habits, creating a buffer against economic uncertainties.

Those curious about how to implement this strategy effectively should consider tracking monthly expenses through apps or budgeting spreadsheets to see where their money goes. Regularly reviewing these expenses can help in adjusting the budget and making necessary changes to ensure adherence. Additionally, setting specific savings goals, like a vacation fund or retirement savings, can motivate you to stick with the plan.

In conclusion, the 50/30/20 budgeting method provides a straightforward template for financial management that is both flexible and achievable. By following this approach, many have found the clarity necessary to put their financial lives in order while also enjoying the moment. With a little discipline and commitment, one can unlock a future of financial stability and peace of mind.

SEE ALSO: Click here to read another article

Implementing the 50/30/20 Budget in Everyday Life

Taking the leap into implementing the 50/30/20 budgeting method can significantly shift how you view and manage your finances. However, simply knowing the percentages is not enough; it is essential to engage practically with this framework in your daily life. Here are some actionable tips to help you stay on track with this budgeting approach.

1. Analyze Your Income and Expenses

To kickstart your 50/30/20 journey, begin by determining your after-tax income. Collect your pay stubs, or, if you are self-employed, calculate what you typically bring in after deductions. Once you have a clear understanding of your total income, it’s time to take stock of your expenditures. Utilize budgeting apps like Mint or You Need a Budget (YNAB) to accurately track and categorize your spending. This way, you can visualize where your money flows.

Once you have data on your spending habits, break down your expenses into the three 50/30/20 categories:

- Needs: Rent or mortgage, utilities, groceries, insurance, minimum debt payments.

- Wants: Dining out, hobbies, entertainment, vacations, and other discretionary spending.

- Savings and Debt Repayment: Contributions to savings accounts, retirement plans, and extra payments towards debts.

2. Set Clear Priorities

Your financial health is a reflection of your priorities. When allocating funds within each category, ask yourself what’s essential and what can wait. For instance, while eating out may bring immediate gratification, redirecting some of that budget towards building an emergency fund can promote long-term peace of mind.

Consider crafting a priority list for both needs and wants. This list can guide you when deciding between different spending options, ultimately keeping you aligned with your budgetary goals. If you find yourself wanting to splurge on concert tickets, check to see if that expenditure aligns with your set 30% limit for non-essential purchases.

3. Regularly Review and Adjust

Your financial situation is not static; fluctuations in income or unexpected expenses may arise. Hence, it is crucial to review your budget monthly or even weekly to ensure it continues to reflect your current financial landscape. More frequent evaluations will help you identify trends in your spending and uncover any areas where adjustments can be made.

During these reviews, ask yourself the following:

- Are there any areas where I overspent?

- Have my needs changed significantly, requiring a reallocation of funds?

- Am I consistently meeting my savings goal?

By remaining proactive about your budget, you can take control of your financial destiny while adapting to both expected and unexpected changes. Embracing the 50/30/20 budget in a practical manner is about much more than simply slicing your income; it’s about enhancing your ability to make deliberate choices about your money and your future.

SEE ALSO: Click here to read another article

Maximizing Your 50/30/20 Budget for Success

Implementing the 50/30/20 budgeting method goes beyond initial tracking; it requires a proactive approach to ensure you are not only following the plan but also getting the most out of it. Here are some strategies to maximize your budget’s impact and unlock the path to financial freedom.

4. Utilize Tools and Resources

Choosing the right tools is vital for effective budgeting. Several apps and software programs can automate the tracking and categorization of your expenses, making it easier to stick to the 50/30/20 framework. Besides the aforementioned Mint and YNAB, consider alternatives like EveryDollar, which allows you to create a budget from scratch, or Personal Capital, which also offers investment tracking features. Using these tools can give you real-time insights into your budget performance, guiding informed financial decisions on the fly.

Additionally, consider utilizing a spending tracker, either in app form or as a spreadsheet. This tool can help you break down your spending habits in greater detail, allowing you to see the minutiae of your financial life and where small changes can add up to significant savings over time.

5. Embrace Automation

Automating your finances can reduce the stress of managing savings and bills. Set up automatic transfers to your savings account or retirement plan right after payday. This takes the decision-making out of the equation and ensures that you’re consistently funneling money into your savings without the temptation to spend it elsewhere. Some banks even offer apps that round up your transactions and deposit the spare change into your savings account, making it easier to reach your goals without feeling the pinch.

Moreover, automate your bill payments to avoid late fees and ensure you never miss a payment. According to a report from the Consumer Financial Protection Bureau, Americans faced over $12 billion in late fees annually, indicating the potential savings involved with automatic payments.

6. Practice Mindful Spending

Implementing the 50/30/20 budget requires a shift in mindset towards mindful spending. Reassess your purchasing mentality by asking yourself whether each purchase aligns with your values and budget. For everyday expenses, consider the 30-day rule: if you’re tempted to buy something outside of your needs category, wait 30 days before making the purchase. This provides ample time to consider whether you truly want or need the item.

Also, look for ways to reduce your needs category. For instance, consider moving to a more affordable housing situation, refinancing loans to lower rates, or shopping for groceries with a prepared shopping list to minimize impulse purchases. Each small reduction can contribute significantly to your overall budget, enabling more funds to be allocated towards savings or debt repayment.

7. Engage in Financial Education

To truly harness the power of the 50/30/20 budget, invest time in financial education. Read books, attend workshops, or follow financial podcasts tailored to enhancing your knowledge about managing money. Understanding concepts of interest rates, investment options, and budgeting strategies can empower you to make educated decisions, ultimately propelling you towards financial stability and independence.

Resources such as “The Total Money Makeover” by Dave Ramsey or “You Are a Badass at Making Money” by Jen Sincero can provide invaluable insights. Accessible online courses from platforms like Coursera or Udemy can also broaden your perspective on personal finance, ensuring that your budgeting efforts translate into long-term success.

By incorporating these practical strategies into your daily life, you can leverage the 50/30/20 budget effectively, ensuring that you’re not only sticking to a plan, but also making meaningful progress towards your financial goals.

CHECK OUT: Click here to explore more

Bringing Your Budget to Life

In conclusion, the 50/30/20 budgeting method is more than just a financial framework; it’s a powerful tool that can guide you toward achieving your monetary aspirations and living a stress-free financial life. By allocating 50% of your income to needs, 30% to wants, and 20% to savings, you create a structured approach that allows you to maintain balance and avoid the detrimental pitfalls of overspending.

However, the true success of this method lies in its practical application. Embracing technology through budgeting apps, automating savings and bill payments, and practicing mindful spending can all significantly enhance your financial management. Each of these strategies not only simplifies adherence to your budget but also encourages you to reassess your financial habits and priorities regularly.

Moreover, engaging in financial education empowers you with the knowledge needed to navigate economic challenges effectively. As you deepen your understanding of personal finance, you will find that the 50/30/20 budget can serve as a foundational pillar for wealth-building, enabling you to make informed, proactive decisions about your financial future.

Begin exploring the resources available, whether books, online courses, or community workshops, and continue to refine your personal budgeting skills. Remember, the path to financial security is not merely about following a plan; it’s about cultivating a lifestyle that aligns with your values and aspirations. By committing to this journey, you’ll not only strengthen your financial health but also unlock a level of financial freedom that enhances your quality of life.

Related posts:

Budgeting tips for couples with different financial styles

How to Create a Reward System that Supports Good Habits with Money

How Loss Aversion Impacts Your Financial Planning

The impact of financial stress on consumption habits

Budget Techniques for Those Living on a Tight Salary

How to develop an investor mindset instead of a consumer mindset

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.